A CRITICAL COMPARATIVE ANALYSIS OF LANGUAGE, INTENT & NARRATIVE

THE SHORT VERSION

There’s a particular species of corporate document that exists not to communicate strategy but to perform it. A kind of expensive theatrical production where the lights go down, the slides go up, and everyone in the room agrees, by unspoken mutual consent, to believe things that the numbers directly contradict. I’ve sat in enough of these rooms. I know the smell.

WPP has now produced two of the most revealing documents in recent advertising history, separated by five years, a collapsed stock price, a new CEO, and approximately seventeen rounds of restructuring. The 2020 Capital Markets Day deck — titled, with the kind of muscular optimism only a recovering holding company can muster, Accelerating Growth — and the 2026 Strategy Update & Preliminary Results presentation, which is trying very hard not to be titled Please Bear With Us.

Read them side by side. Not for the numbers. Not for the strategy. For the narrative. Because what you find, laid out with unintentional honesty across nearly two hundred slides, is that WPP has been giving essentially the same presentation for five years. The vocabulary has changed — “AI,” “WPP Open,” “Enterprise Solutions” have replaced “ecommerce,” “programmatic,” “AKQA” — but the underlying argument is structurally identical: we are too complex, we need to simplify, we are investing in growth, creativity is at our core, the market is big, trust us. The most damning thing about placing these two documents side by side is not what changed. It is what didn’t. The fonts are slightly different. The CEO is a different person. And yet…

Let’s start where both documents start. With the diagnosis.

IDENTICAL SELF-AWARENESS, IDENTICAL FAILURE TO ACT

In 2020, Mark Read stood up and told investors what had gone wrong in 2018. “Negative growth for four quarters. No growth in the USA since Q4 2016. Five or six out of six peers in relative growth.” The company had nine separate creative or digital networks, at least five hundred brands, debt approaching £5 billion, and its largest client under review with “$4 billion of client business being pitched.” This was the crisis. And the message was: we identified it, we acted, we’re recovering.

Now look at the 2026 document’s self-diagnosis. “We have not consistently kept pace with the evolving needs of our clients.” Four pillars of failure called out cleanly: strategic execution, organisational structure, client proposition, portfolio discipline.

The language softens between the two documents — that’s interesting in itself. In 2020 they named numbers. In 2026 the admission is fuzzier, more cushioned in corporate syntax. But strip the wording back and you’ve got the same disease presenting itself for the second time in eight years. Too complex. Too siloed. Not client-centric enough. Structurally inefficient. The patient was told they were cured. They weren’t.

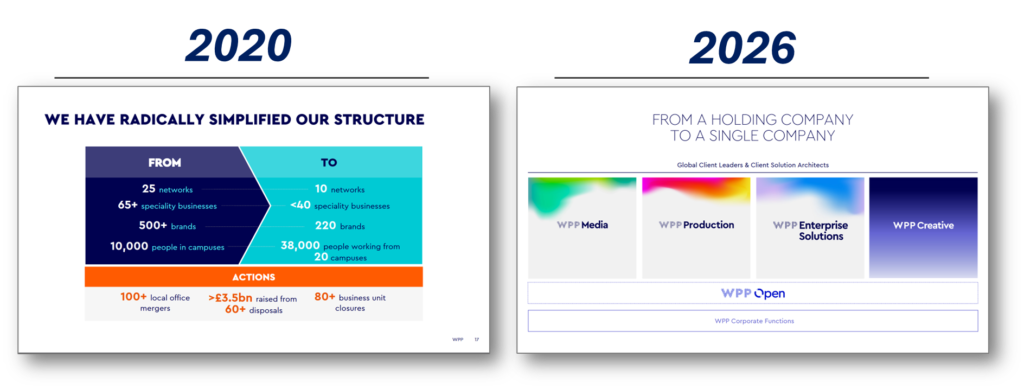

THE SIMPLIFICATION PROMISE: STILL SIMPLIFYING, ALWAYS SIMPLIFYING

Here is the number that should stop anyone who works in or around the holding company model cold.

In 2020, WPP celebrated its simplification achievement with genuine swagger. They had gone from twenty-five networks to ten. From five hundred-plus brands to two hundred and twenty. They had executed over one hundred local office mergers, closed eighty-plus business units, and moved thirty-eight thousand people into twenty campuses. This was the turnaround. This was proof.

By 2026, those very mergers — VML, Burson, the simplification of WPP Media — are being cited as sources of structural cost savings, with headcount falling from approximately one hundred and eight thousand to ninety-nine thousand. Which means the 2020 round of simplification either didn’t simplify enough, or created new complexities that needed solving, or both. And now they’re announcing another one. £500 million of gross savings to be delivered by 2028, covering new operating model design, structural overhead cost savings, and rationalisation and simplification of real estate and long-tail efficiencies.

The categories are word-for-word identical to 2020. Operating model. Real estate. Shared services. Procurement. The 2020 document targeted £600 million of annual gross cost savings by 2025. The 2026 document doesn’t acknowledge this target or its outcomes. It just announces a new one.

This is what institutional amnesia looks like when it’s dressed in a presentation template.

THE FINANCIAL NARRATIVE: FROM OPTIMISM TO DAMAGE CONTROL

Let’s talk about the promises. Because this is where the two documents diverge most sharply, not in argument, but in mood. And the gap between them is the story.

The 2020 financial plan was written in a major key. Core growth of one to two percent, P&L investment rising to £400 million annually by 2025 to drive incremental one-and-a-half percent growth, M&A of £200 to £400 million annually adding another half to one percent. The explicit target: a headline operating margin of 15.5 to 16.0 percent by 2023, and revenue less pass-through costs growing at three to four percent annually from 2023 onwards.

The 2026 document is the accounting of what actually happened. Like-for-like net sales declined 5.4 percent. Headline operating margin: thirteen percent — down two percentage points from the prior year. Headline diluted EPS down 28.4 percent. The declared final dividend was 7.5 pence, for a full-year total of 15.0 pence, compared to 39.4 pence the year before. That’s a sixty-two percent cut in dividend. The 2026 guidance is not a recovery narrative — it’s triage: “down mid to high-single digits in the first half of 2026 with an improving trajectory in the second half.”

None of the 2020 targets were met. Not one. The margin aspiration of 15.5 to 16.0 percent for 2023 arrived in 2026 as thirteen percent and falling. The three to four percent growth target became a 5.4 percent decline. But you won’t find a slide in the 2026 deck that puts these two sets of numbers next to each other and accounts for the distance between them. The analysts in the room know. But no one says it out loud.

That’s a choice. And choices like that have a cost.

TECHNOLOGY & DATA: THE NOUN CHANGES, THE VERB DOESN’T

Now the technology argument. This is where the narrative performance is most naked.

The 2020 deck led its technology credentials with: approximately thirty billion dollars in annual GMV over WPP-installed commerce platforms, a 1.6 billion audience pool updated daily for planning and activation, more than twenty thousand technology accreditations in 2020, and a top-three global partnership with Adobe and Salesforce in marketing technology. Ten billion dollars in client billings across Google, Amazon and Facebook.

The 2026 deck leads its technology credentials with WPP Open, Open Intelligence, and AI transformation. The Adobe partnership is still there — explicitly called out five years later as a key pillar of the strategy.

Think about that for a second. The same partnership. Featured as the proof point in 2020, and still the proof point in 2026. The product has changed — “WPP Open,” “Open Intelligence,” generative AI — but the rhetorical move is identical. We have proprietary technology infrastructure that differentiates us from our competitors. In 2020 that was sold through programmatic and data pools. In 2026 it’s sold through AI and platform integration. The noun changes. The verb stays the same.

What is genuinely new in 2026 is Enterprise Solutions — a named strategic pillar targeting a two hundred and thirty billion dollar addressable market in consulting, CX, and technology implementation. This positions WPP to compete with Accenture and Deloitte in a way the 2020 deck doesn’t. It’s real differentiation, or the aspiration of it. The foundations exist — approximately ten thousand people, around $1.8 billion in revenue, eighty-plus top-100 clients served, and strong Forrester and IDC rankings. But between foundation and strategy there’s a lot of air. WPP has been talking about “Experience, Commerce and Technology” growing to forty percent of revenues since 2020. It’s 2026 and they’re announcing a new framework for trying.

CREATIVITY: THE PERENNIAL PROMISE

The creativity argument. This one’s interesting because of what disappears.

The 2020 deck was brimming with creative trophies. Cannes Lions Holding Company of the Decade. Most Effective Holding Company 2012 to 2020. Number-one media holding company for three years running, according to WARC. Eighty-nine Clio Awards in 2019, with top honours to Ogilvy and AKQA.

The 2026 deck describes WPP Creative as “home to our iconic agency brands,” with “simpler client navigation, democratised modern marketing capabilities, true integration with WPP Media and WPP Production, and a competitive cost base.”

The awards vocabulary has vanished. What replaces it is the language of structure and integration. Whether that’s strategic maturity — moving from awards metrics to client outcome metrics — or whether it signals that the creative reputation has eroded along with the business performance, I genuinely can’t tell. Possibly both. The thing about awards in this industry is that they’re lagging indicators. They measure yesterday. But their absence in 2026 is its own data point.

THE CULTURE SLIDE: UNCHANGED IN SUBSTANCE

The culture section of both documents is, honestly, a little heartbreaking to read in sequence.

2020: employer of choice for all, modernisation of experiences, growth. A commitment to investing thirty million dollars in racial equity over three years. A new Inclusion Index. Partnerships with Valuable 500, Unstereotype Alliance, LaGrant Foundation. Signatory of Women’s Empowerment Principles.

2026: future-facing skills development, aligned incentives, career mobility and progression, performance management and accountability, frequent and clear communication, a new mission and growth mindset.

The thirty million dollar racial equity commitment from 2020 is nowhere in the 2026 document. Neither are the specific diversity partnerships. This is not accidental. Global corporate discourse on DEI shifted hard between 2023 and 2026, and WPP has moved with that current. I’m not making a political argument about it here — just noting that five years ago this was centred explicitly, with money attached to it and specific external partnerships named. Now it’s folded into “high-performance culture” and “career mobility.” That word “accountability” is doing a different kind of labour in 2026 than it did in 2020.

BONUS:

THE LEXICAL AUTOPSY: WHAT WPP’S WORDS ARE ACTUALLY DOING

I took a further lexical n-gram-ish look into the key terms (and the frequency of appearance) adjacent to the words “growth“, “transformation” and “future“.

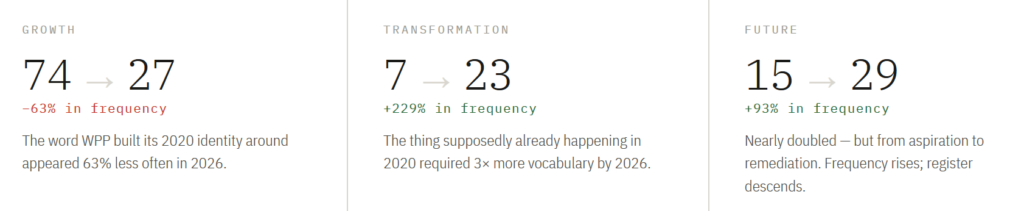

GROWTH

2020: 74 appearances. 2026: 27 appearances.

That number alone is a eulogy. In 2020, “growth” was the oxygen in the room — the word that everything else organised itself around. It appeared 74 times, and the adjacent vocabulary tells you exactly what kind of growth they were imagining. “Accelerating” (10 times), “accelerated” (9 times), “investment” (11 times), “higher” (6 times), “medium-term” (5 times), specific geographies like “India” (5 times), and a very specific number — “400m” (5 times) — appearing in the company of “growth” like a promise with a price tag attached.

In 2026, “growth” appears 27 times. Sixty-three percent less frequently. And look at what sits next to it now: “return” (4 times), “savings” (3 times), “gross” (3 times), “drivers” (3 times), “portfolio” (3 times), “performance” (3 times). “Savings” in the company of “growth.” That is not a growth story. That is a cost story wearing a growth story’s clothes.

The most telling adjacency in 2026 is “superior” — appearing 3 times next to “growth.” “Deliver superior growth for clients” is one of WPP’s four stated 2026 strategic objectives. “Superior” is an interesting word to reach for when your LFL net sales just declined 5.4 percent. It is aspirational in the most technical sense: it describes a condition that does not yet exist. In 2020, they used “accelerating.” In 2026, they’ve retreated to “superior.” “Accelerating” implies motion already underway. “Superior” implies a quality you intend to achieve. The distance between those two words is five years of underperformance.

The self-referential nature of “growth” adjacent to itself — 18 times in 2020, 6 times in 2026 — is also telling. In 2020, growth was the answer to growth. “Growth strategy,” “growth markets,” “growth areas,” “growth platforms” — the word was recursively embedded in its own logic. We will grow because we are growing. By 2026, that recursion has broken. Growth no longer refers to itself. It refers to what needs to be rebuilt.

TRANSFORMATION

2020: 7 appearances. 2026: 23 appearances.

This is the reversal. The word nobody used much in 2020 — when things were supposedly already transforming — has tripled in the vocabulary by 2026, precisely because the transformation didn’t happen.

In 2020, “transformation” appeared 7 times, always in the same phrase: “group-wide transformation programme.” The adjacent terms were structural and managerial: “group” (5 times), “wide” (4 times), “programme” (4 times), “margins” (3 times), “improved” (3 times). This was transformation as an internal efficiency exercise — something you do to your cost base, not your identity. The word carried no particular urgency. It was one of four pillars in a financial plan.

By 2026, “transformation” appears 23 times — more than three times as frequently — and the adjacent vocabulary is completely different. “Partner” (18 times), “clients” (18 times), “data” (10 times), “media” (8 times), “lead” (8 times), “simplify” (8 times), “enterprise” (3 times), “solutions” (3 times). The transformation is no longer internal. It is now client-facing. “Partnering with clients on AI transformation” is the new formulation. The word has migrated from the finance section of the deck to the strategy section. From a savings mechanism to a value proposition.

This is either genuine strategic evolution — WPP positioning itself as the agent of transformation for its clients rather than simply for itself — or it is a vocabulary upgrade that describes the same structural ambition in more marketable terms. The honest answer is probably both. “AI transformation” is a real market opportunity. It is also a phrase that sounds better than “we need to cut overheads and merge agencies again.”

The most significant adjacency shift: in 2020, transformation sat next to “margins” and “improved.” In 2026, it sits next to “partner” and “clients” 18 times each. Same word. Completely different facing direction. In 2020, transformation looked inward. In 2026, it looks outward. Whether the organisation has actually reoriented to match the vocabulary is the unanswered question.

FUTURE

2020: 15 appearances. 2026: 29 appearances.

“Future” almost doubles between the two documents. But the nature of what “future” means changes so completely that the frequency comparison is almost misleading. You need to look at what lives next to it.

In 2020, “future” sat primarily next to “model” (8 times) and the paired terms “today/current” (4 and 3 times respectively). “Future model” versus “model today” — this was the recurring structure of the 2020 transformation slides. The comparison table. Column A: what we have now. Column B: what we’ll have then. “Future” in 2020 was a destination column on a slide. Adjacent terms included “creativity” (3 times) and “better” (3 times) — which together form WPP’s stated purpose, “using the power of creativity to build a better future,” appearing in both decks’ culture sections verbatim.

In 2026, “future” has a different fixed companion. “Firm” (21 times), “financial” (21 times), “foundations” (21 times). “Create firm financial foundations for the future” is one of WPP’s four 2026 strategic objectives, and it appears repeatedly throughout the deck as a navigational element, which mechanically inflates these adjacencies. But the choice of what to call a strategic objective is itself a choice. They could have said “deliver financial strength” or “restore financial performance.” They said “firm foundations for the future.”

“Foundations” is a word you use when you’re building from scratch. Or when what was there before has subsided. “Firm” is a word you use when the ground has been unstable. “Future” in 2026 is no longer a destination column — it’s a promise of basic structural stability. The aspirational register of “better future” (2020) has become the remedial register of “firm financial foundations” (2026).

The movement from “future model” to “firm foundations for the future” is, lexically, a descent. In 2020, the future was a designed state you were moving toward with intention and investment. In 2026, the future is something you need solid ground to reach at all.

THE PATTERN UNDERNEATH THE PATTERN

Put these three words together and you get a coherent, unintentional narrative that neither document would endorse individually.

In 2020: Growth is accelerating through investment. Transformation is an internal programme improving margins. Future is a designed destination model we’re building toward.

In 2026: Growth must be returned to, via savings. Transformation is what clients need and we will partner with them to deliver. Future requires firm financial foundations before we can discuss it further.

The 2020 document speaks with the grammar of someone running. The 2026 document speaks with the grammar of someone who fell, got up, and is now walking carefully, watching the ground.

What the lexical data captures that the individual presentations obscure is the direction of travel. Read any single document and you can make a reasonable case for the strategy. Read the word frequencies across both and you see something the slides are not designed to show you: an organisation that spent five years talking about the future in confident, investment-heavy terms, and arrived in 2026 needing to create firm foundations for it first.

The words knew before the slides would say it.

THE MARKET OPPORTUNITY ARGUMENT: BIGGER NUMBERS, SAME LOGIC

So here’s what bothers me most, sitting with both of these documents.

WPP is run by some very smart people. It employs some of the most analytically gifted people in the communications industry. It has access to more market intelligence than almost any organisation on earth. Its strategy documents are well-constructed, internally coherent, and full of the right kinds of market data. The 2026 deck identifies the global agency and transformation services market as expected to exceed five hundred billion dollars by 2028, growing at a five percent CAGR. The TAM is real. The opportunity is real. But the incisiveness is, sadly, underwhelming.

The company that produced the 2020 Capital Markets Day deck could not execute against its own plan. Five years of relative underperformance, one catastrophic 2025 (a 5.4 percent LFL decline, a 28.4 percent EPS fall, a dividend cut of sixty-two percent), and a 2026 deck that opens with “we have not consistently kept pace with the evolving needs of our clients.” The gap between strategic articulation and strategic execution at WPP isn’t a knowledge problem. The analysis is fine. The presentations are polished. The market understanding is legitimate.

The failure is institutional. It is the gap between knowing and doing that every large, legacy organisation faces, and that few actually close. The irony that would not be lost on anyone familiar with my ANTIGENERIC thesis is that WPP — the world’s largest creative services conglomerate, the company whose agencies exist to help their clients break through commoditisation and sameness — has itself become generic in the most fundamental way possible. It has become an organisation that produces the same strategic response to the same structural crisis, on a five-year cycle, with slightly updated vocabulary and slightly worse numbers.

The 2020 deck was titled Accelerating Growth. The 2026 deck has no title as bold as that. Its working title might as well be: Still Trying. To their credit, the 2026 document is more honest than its predecessor about the severity of the situation. The self-indictment is real. The three-phase plan — Stabilise, Build, Accelerate across 2026, 2027 and 2028 — is more methodical and measurable than 2020’s aspiration curves. The KPIs are harder: new business wins, client retentions, revenue per head, cost savings, leverage, and LFL net sales growth sitting alongside leading and lagging indicators in a structured accountability framework.

But I’ve read the 2020 version of that too. The specific words are different. The architecture is the same.

The only genuinely new strategic bet in 2026 — and I think it might be a good one — is the shift from holding company to single company, with WPP Media, WPP Creative, WPP Production, and WPP Enterprise Solutions as distinct capability pillars under one roof, coordinated by Global Client Leaders and Client Solution Architects. That structural logic didn’t exist in 2020. It’s a real change if they execute it.

If.

And that “if” is carrying five years of weight.

A LAST WORD

WPP is not uniquely guilty here. The holding company model as a whole is going through a reckoning it’s been deferring since the first wave of consultancy-as-agency competition in the mid-2010s. The market shifted. The clients got smarter. The production economics changed. The creative monopoly crumbled. Every WPP competitor is running some version of the same play: simplify, integrate, invest in technology, grow in faster-moving categories, tell your clients you’re a growth partner now, not just a service vendor.

What makes WPP’s two documents so instructive is the specificity of the gap between promise and delivery, and the institutional courage — or perhaps institutional necessity — of going back to analysts with the same framework and asking them to believe again.

They might. The market is big enough. The brands are real. The talent is there.

But somewhere in a filing cabinet, or more likely in a shared drive that nobody’s reorganised since 2021, the 2020 deck is sitting there. And it remembers.

Sid out.

.

.

.

.

BONUS: LEXICAL ANALYSIS IN TWO PARTS

PART 1: THE VANISHING ACT: HOW WPP STOPPED TALKING ABOUT PEOPLE

A comparison of how the words “people” and “talent” appear in WPP’s Capital Markets Day 2020 and Strategy Update 2026 — their frequency, adjacency, and what the shift reveals about the organisation’s relationship with its workforce.

THE RAW COUNT

| 22 → 0 “People” appearances 2020 → 2026 | 11 → 18 “Talent” appearances 2020 → 2026 | −100% Word “People” completely absent in 2026 |

That zero is not a rounding error. The word “people” — which appeared 22 times in 2020, had its own dedicated section, its own strategy slide, and its own KPI framework — does not appear once in the 2026 document.

PEOPLE MATTERED IN 2020

In 2020, “people” carried genuine weight. The dedicated section on page 52 was titled:

“Our People Are Our Company: The Best Talent Delivering for our Clients”

A statement that treated people as the primary asset, not a supporting pillar. The three-part people strategy was explicit: Attraction, Retention, Growth.

Specific commitments with numbers attached

- 100k+ employees described as “highly skilled and motivated”

- Strong COVID response cited as evidence of people resilience and commitment

- 60–65% of hires coming from outside WPP flagged as a problem to fix

- £30 million racial equity commitment over three years, diversity data published annually

- New Inclusion Index to track belonging and inclusion experience

- Partnerships with Valuable 500, Unstereotype Alliance, LaGrant Foundation

- Target of 85,000 people in 65 cities on campus by 2025

- New technology described with a “people-first lens”

- £150m of the £400m annual investment explicitly allocated to talent

Five explicit KPIs listed for people

- Satisfaction & wins metrics

- Learning and certification metrics

- Attrition / churn metrics

- Productivity and client impact metrics

- Mobility and career progression metrics

The talent language in 2020 was equally grounded: diversity and equity embedded into talent processes, early career diverse talent pipelines, career frameworks for development and succession. These commitments had named owners — Jacqui Canney, then Chief People Officer — and line items in the financial plan.

THE 2026 – NOT A SINGLE MENTION OF “PEOPLE”

“People”: zero. Gone entirely.

“Talent” appears 18 times — but 14 of those 18 appearances are navigational repetitions of a single strategic objective repeated across every section divider slide in the 112-page document:

“Drive a high-performance culture and attract and retain the world’s best talent”

That phrase appears verbatim on navigation slides throughout. It is a menu item, not a chapter. Strip the navigation repetitions and “talent” as substantive content appears on exactly two slides.

What those two slides actually contain

- Future-facing skills development

- Aligned incentives

- Career mobility and progression

- Performance management and accountability

- Frequent and clear communication

- New mission and growth mindset

No numbers. No named commitments. No investment quantum. No DEI framework. No KPIs. No named HR lead. The £30m racial equity pledge is not referenced. The Inclusion Index is not referenced. The 85,000 campus target — not mentioned or accounted for.

THE NARRATIVE SHIFT, PRECISELY DESCRIBED

In 2020, the people narrative was evidential — it came with data, money, named external partners, accountability metrics, and a named executive responsible. It treated culture as something you build, track, and invest in.

In 2026, the people narrative is aspirational and frictionless. “High performance culture,” “world’s best talent,” “aligned incentives,” “growth mindset.” These are phrases that describe a desired state without specifying the cost, the mechanism, or the measurement of getting there.

People are inside the organisation — they have experiences, they churn, they need career frameworks and inclusion indices. Talent is outside it — something you compete for in a market, a resource to attract and retain. The 2026 document has stopped talking about the humans inside WPP and started talking about the category of human it wants to acquire.

SIDE-BY-SIDE: PEOPLE & TALENT ACROSS BOTH DECKS

| Dimension | 2020 Capital Markets Day | 2026 Strategy Update |

| People appearances | 22 | 0 |

| Talent appearances | 11 | 18 |

| Dedicated section | Yes — “Our People Are Our Company” | No dedicated people section |

| People strategy | 3-pillar: Attraction, Retention, Growth | Not named as standalone strategy |

| Financial commitment | £150m of £400m investment in talent | No quantum specified |

| DEI framework | £30m racial equity; Inclusion Index; named external partners | Not referenced |

| Named HR lead | Jacqui Canney (named) | Not named |

| KPIs listed | 5 explicit people KPIs | None listed |

| Campus target | 85,000 in 65 cities by 2025 | Not mentioned |

| Dominant framing | People as asset inside the org | Talent as market category to compete for |

WPP is not unique in this shift. The broader 2025–26 corporate retreat from DEI commitments is well documented, and the language of “high-performance culture” has become the preferred substitute across many holding companies and professional services firms. The specifics have been replaced with the aspirational. The commitments have been replaced with the directional.

What makes WPP’s case instructive is the precision of the gap. Not a softening of language — a complete erasure of a word. Twenty-two appearances to zero. And the simultaneous inflation of “talent” from 11 to 18 appearances, almost entirely as a navigational label rather than substantive content.

The headcount fell from approximately 108,000 to 99,000 in the same period. The dividend was cut 62%. The people who remained inside WPP went from being the subject of a dedicated strategy with named owners and explicit KPIs to being absent from the vocabulary entirely. Whether that is a deliberate signal or an editing oversight is, itself, a strategic communication.

The word that humanised the 2020 strategy has been quietly removed from the 2026 one. Twenty-two times to zero. That’s not an editing choice. That’s a posture.

PART TWO: USE OF “GROWTH”, “TRANSFORMATION” AND “FUTURE” AND ADJACENCIES

The words

knew first.

| Word | 2020 — top adjacencies | 2026 — top adjacencies | What shifted | |

|---|---|---|---|---|

| growth | INVESTMENT · ACCELERATING HIGHER · £400M · MARKETS |

→ | RETURN · SAVINGS SUPERIOR · DRIVERS |

From investment as engine to savings as substitute. The word faces backward. |

| transformation | GROUP · PROGRAMME MARGINS · IMPROVED |

→ | PARTNER · CLIENTS DATA · SIMPLIFY |

From inward efficiency to outward service pitch. Same ambition, different audience. |

| future | MODEL · TODAY CREATIVITY · BETTER |

→ | FIRM · FINANCIAL FOUNDATIONS · UNLOCK |

From aspirational destination to structural precondition. A descent in register. |

WPP Capital Markets Day, Dec 2020 · WPP Strategy Update & FY25 Results, Feb 2026